I decided months ago not to write about the looming infrastructure bill Democrats are hoping to pass through Reconciliation until it was up for a vote.

Both Houses in Congress are working to agree on a $3.5 Trillion bill that would “dramatically expand America’s social safety net.” [quote] Many proposals affect health care, but until we know what stays in the bill and what ends up on the cutting room floor, it doesn’t make sense to analyze it.

Until now.

Both the House and Senate versions aim to circumvent the 12 States that haven’t expanded Medicaid by offering a federally backed alternative to the residents that qualify in those states.

Congress can’t do that. I’d like to explain why.

The ACA Plan

To understand what’s happening in Congress now, we need to start with a summary of the Expansion of Medicaid design in the Affordable Care Act [“Obamacare”]. One of the primary goals of the ACA was to get Americans insured. When President Obama signed the ACA (March 2010), 16% of Americans were not insured, with gaps in health care and prevention as a result.

The ACA increased the number of insured Americans dramatically; by 2016, only 9% of Americans lacked coverage, 20 million Americans were newly insured by 2020. [source]

The law achieved those gains through a three-layer-cake strategy to address the uninsured at all levels of the economy:

- employers with more than 50 workers were required to offer coverage (employee coverage had declined over the years, with only 55.9% of Americans insured through their jobs by 2012);

- entrepreneurs, small companies, and individuals who did not have benefits through employment were given access to group discounts through the Obamacare “Exchanges” (also known as “Marketplaces”) in each state (with federal stipends available on a sliding scale to help with premium costs);

- People who could not afford to buy a policy on the Exchanges (even with a subsidy) became eligible for Medicaid under a new definition offered by the ACA. Medicaid (jointly controlled by the Federal & State Governments) would now cover all people with incomes at or less than 133% of the federal poverty level. (This figure may vary by state and calculation, source).

The Expansion of Medicaid was crucial to the ACA framework. To this point, states had different terms for eligibility- some were quite generous (ex: California), whereas other states did not cover most poor people between the ages of 18 & 65 (ex: Texas).

In return for changing their eligibility requirements under the ACA, the Federal government assumed all the costs associated with people added to a state’s Medicaid rolls for the first 3 years, followed by increasing state participation incrementally with a cap at 10% of costs (i.e., under the ACA the Federal support to a state that expanded Medicaid would be 90% of those additional costs indefinitely.)

The US Supreme Court Tears Apart the Plan

The first challenge to the constitutionality of ObamaCare was NFIB v Sebelius, decided on June 28, 2012. That case is best known as the 5-4 Opinion by Chief Justice Roberts that saved the ACA by holding that the Individual Mandate is Constitutional.

However, in that same Opinion, the ACA lost and lost badly. By a vote of 7-2 (only Ginsberg & Sotomayor dissenting), the Court denounced the ACA “coercion” on the states to Expand Medicaid (the law used the ability to distribute federal funds- or not- as an incentive).

Here is the Supreme Court’s point: Expanding Medicaid is a States’ Rights Issue. Period.

Twenty-Four states initially said “No!” to Medicaid Expansion after the NFIB decision. Concerns about the cost of the 10% funding, fear that the Federal Government might renege on its promise, and fundamental questions about federalism were commonly cited reasons for the states opting out.

Twelve States Changed Their Minds: Why?

Interestingly, after strident rejection after the NFIB case (and the grave injury to the ACA plan), a dozen states that grabbed at the independence offered by the Supreme Court decided to reverse course.

Between 2012 and 2020, these 12 states, predominantly under Republican leadership, came on board (through various mechanisms, sometimes with waivers from CMS, and with varying levels of success). A map of what states have Expanded Medicaid is available here.

Why are states changing their position?

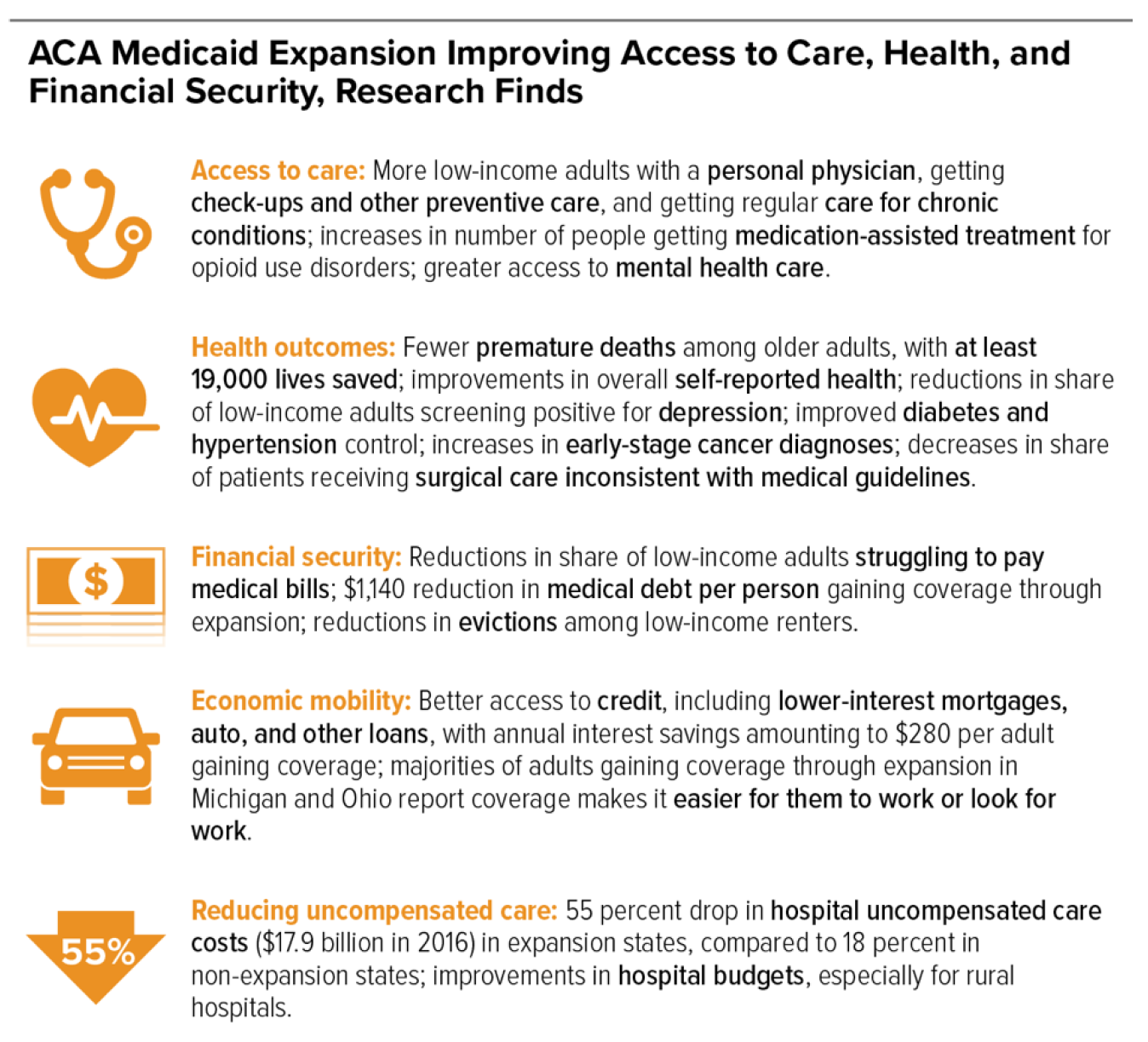

After more than a decade, the impact of Medicaid Expansion is evident through research. A compilation of those studies by the Center on Budget and Policy Priorities [CBPP] demonstrates:

States are changing their position because Medicaid Expansion works.

So… Why Can’t Congress Make This Happen Everywhere?

I know that was a very long walk around the barn- my point is there are good reasons why Democrats in D.C. would love to finish the ACA plan all these years later. For the first time, ObamaCare would be fully implemented, and 4.4 million working poor Americans would get insured, many for the first time since becoming adults.

And the timing is perfect! We now know (after 11+ years) that ObamaCare is here to stay (the latest Supreme Court ruling making that clear with a 7-2 vote undermining the legitimacy of the challenge from the outset).

But even if Expansion is the right thing to do (and I say that knowing there is a strong minority opinion that it is not), that doesn’t mean Congress can do it.

More importantly, there are enormous jurisdictional issues with Congress meddling in Medicaid Expansion within the states.

To start, there is the ugly reality of funding. To get enough money to bring Medicaid Expansion to the last dozen states, Democrats in Congress are now considering cutting commitments to improve Medicare from the Infrastructure Reconciliation Bill. Adding dental, vision, and hearing benefits to Medicare was promised to beneficiaries (and revising Medicare, which is exclusively under Federal control, doesn’t raise any jurisdictional issues). Robbing Medicare to chase after Expansion in recalcitrant states isn’t only politically risky, it’s also unfair.

More importantly, there are enormous jurisdictional issues with Congress meddling in Medicaid Expansion within the states.

Let me reiterate: As the Supreme Court said in 2012, Expanding Medicaid is a States’ Rights Issue. (If Congress passes Federal Expansion of Medicaid in the 12 “hold-out” states, another Supreme Court challenge is inevitable.)

However, even if the the Supreme Court isn’t an issue, it is a core truth in our system of federalism that control over health care is reserved to the states. The “Police Powers” (protecting the health, safety, welfare, and morals of the people) represent the inherent duties of government and were never relinquished by the states. (See Fontenotes No. 91 for more on the Police Powers and the division between state and federal authority.)

If the Supreme Court and the Police Powers don’t make a strong enough argument for state control over Medicaid Expansion, the Tenth Amendment is the final stroke against Congressional overreach:

The powers not delegated to the United States by the Constitution, nor prohibited by it to the States, are reserved to the States respectively, or to the people.

What Happens Next?

We wait.

We wait until the populations (i.e., voters) in the last dozen states decide it’s time to take on Expansion. And we may not have to wait long. A poll this year in Texas revealed “69% of Texans say the state should expand Medicaid to provide health insurance to low-income people who are uninsured” [source], in 2020 three-quarters of North Carolinians supported Expansion [source], 69% of likely 2022 voters in Alabama want Expansion (including 50.6% of Republicans) [source], an April poll in Florida showed 54% of voters support Expansion in that state (with only 29% firmly opposed) [source], and a 2021 state-wide poll in Tennessee showed three times more voters (63%) supported Expansion than opposed (21%) that state’s initiative [source].

I’m not saying these last 12 conversions will be painless or quick; Medicaid itself took 17 years to become a national program! (Although passed in 1965, Arizona did not adopt that “new” program until 1982.)

However, the trajectory of Medicaid Expansion is clear. It will happen. Someday, we will achieve the Affordable Care Act’s vision of a fully insured America.

Until then, Congress, Stay in Your Lane!

Want to Know More?

The cost of having Covid is going up. Since March 2020, most private insurers have written off Covid hospitalizations and ER visits (i.e., patients have not had to pay their co-payments and deductibles). This was a commendable and largely voluntary effort on the part of the insurance industry. But that altruistic endeavor is coming to an end. As the pandemic continues, and 97% of hospitalized patients are unvaccinated, insurance companies are “now treating Covid more like any other disease, no longer fully covering the costs of care.” [quote] (Examples: Aetna stopped writing off bills beginning March 2021; United Health Care also stopped in March. source.) For patients with high deductible insurance policies, this means costs associated with Covid could easily reach the average deductible of $2,303 out-of-pocket for the patient.

2. The cost of Covid hospitalizations is staggering. The average hospitalization is $20,000 (Kaiser) but complex stays (requiring long-term intubation, ECMO, and ICU care) this summer were $320,000 per patient (MedPage Today).

Private and Governmental insurance (Medicare, Medicaid, etc.) reimburse hospitals for the bulk of Covid costs, but on a negotiated scale. Worse yet, uninsured patients (such as the uninsured poor in Non-Medicaid Expansion states) aren’t covered at all. These “bare” patients are most likely to appear in hospitals run by local municipalities or counties (at tax-payer expense) and in rural, underserved communities. The Cares Act under the Trump Administration included $100 billion to support health care providers, including hospitals treating uninsured patients. Increasingly, however, uncompensated Covid care is falling directly on public and rural hospitals, already at risk of closure. In 2019 these hospitals absorbed most of the $41.6 billion uncompensated care in our country, and that was pre-pandemic.