More than a month ago, I set out to explain why I strongly encourage people to stay away from Medicare Advantage (“Medicare Choice” or “Medicare C”) plans.

In Part I of this series, I described traditional Medicare in detail as a guide for readers making coverage decisions and as a prelude to explaining how Medicare Advantage is dramatically different.

In Part II, I explained cost-cutting in the private insurance industry through Utilization Management, how Medicare Advantage plans are paid, the politics behind privatizing Medicare, and why Medicare Advantage is the private insurance industry’s “hottest” market.

I can now provide more detail on my five major complaints about Medicare Advantage, as I have been promising throughout this series.

1. Through Utilization Management, Medicare Advantage is more likely to delay or deny your medical care

Although the names sound similar, a person on traditional Medicare has coverage for their medical care through the federal government (CMS). In contrast, a person with Medicare Advantage has a policy with a private insurance company, which is, in turn, paid for by the feds (see Part II).

Private insurance companies make decisions on reimbursement for a patient’s care (both what they will pay for and for how long) through a series of tools collectively known as Utilization Management (see Part II). This decision-making process is in the hands of the insurance company, not the patient’s doctor or provider.

Because the private company (and shareholders) can retain any of the set monthly funds allotted to carry a beneficiary, Medicare Advantage plans are incentivized to deny or delay coverage for the care ordered for a patient. And they do. A lot.

A Federal investigation last April reported that approximately 13% of patient care denied by Medicare Advantage plans would have been covered by traditional Medicare, meaning “as many as 85,000 beneficiary requests for prior authorization of medical care were potentially improperly denied in 2019.” [quote, emphasis added] The inspection of Medicare Advantage payment practices revealed “widespread and persistent problems related to inappropriate denials of services and payment.” [quote]

The denials may, in effect, be attempts to delay payment with the expectation the cost will be prevented; another federal investigation in 2018 demonstrated that 75% of denied claims were reversed if the patient appealed (few people do, presumably because they don’t know they can).

Home health services and post-acute skilled nursing or inpatient rehabilitation facility care are more frequently denied by Medicare Advantage plans, such as when a surgeon wants a post-operative patient to have care in a nursing facility rather than go home. [source] Sometimes, if the care is covered, it won’t be in the patient and physician’s choice institution. Traditional Medicare patients are more likely to receive treatment at the highest-quality skilled nursing facilities and home health agencies” than Medicare Advantage patients. [source]

Radiology services such as MRIs and CT scans are also more likely delayed or denied in MA plans. A 2022 investigation by the OIG at HHS provides these two examples:

In one case, an Advantage plan refused to approve a follow-up MRI to determine whether a lesion was malignant after it was identified through an earlier CT scan because the lesion was too small. The plan reversed its decision after an appeal… In another case, a patient had to wait five weeks before authorization to get a CT scan to assess her endometrial cancer and to determine a course of treatment. Such delayed care can negatively affect a patient’s health, the report noted. [quote]

Medicare Advantage patients diagnosed with cancer are also less commonly treated at the highest-rated cancer care hospitals. [source]

2. Medicare Advantage Plans are less likely to cover care from your preferred medical team

Most physicians in America accept traditional Medicare patients with Medigap insurance (see Part I); in 2022, that included at least 80% of physicians across most specialties and 96% of surgical subspecialties. [source] There might be differences between Medigap policies, but as a general rule, reimbursement is available for any Medicare-participating physician a traditional Medicare patient picks.

In contrast, as part of their cost-saving measures, Medicare Advantage plans typically limit their beneficiaries to a defined network of providers [source], such as within an HMO or PPO. If a patient seeks care outside of the network, they will incur additional out-of-pocket costs. [source].

“The biggest disadvantage of Medicare Advantage plans is the closed provider networks, limiting your choice of which doctor or medical facility to use.” [quote, emphasis added]

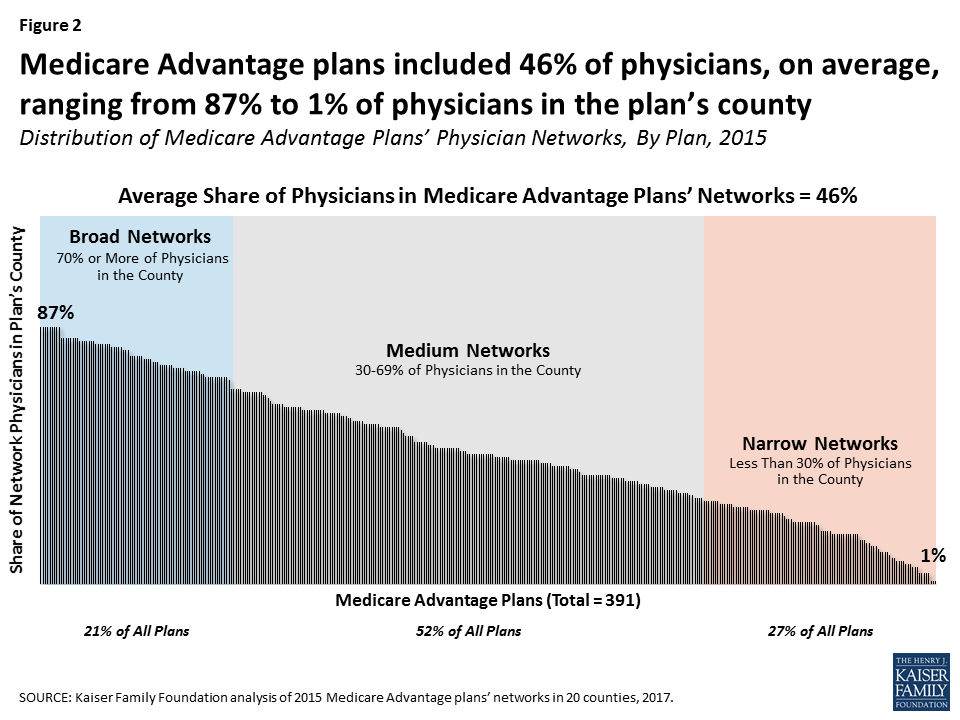

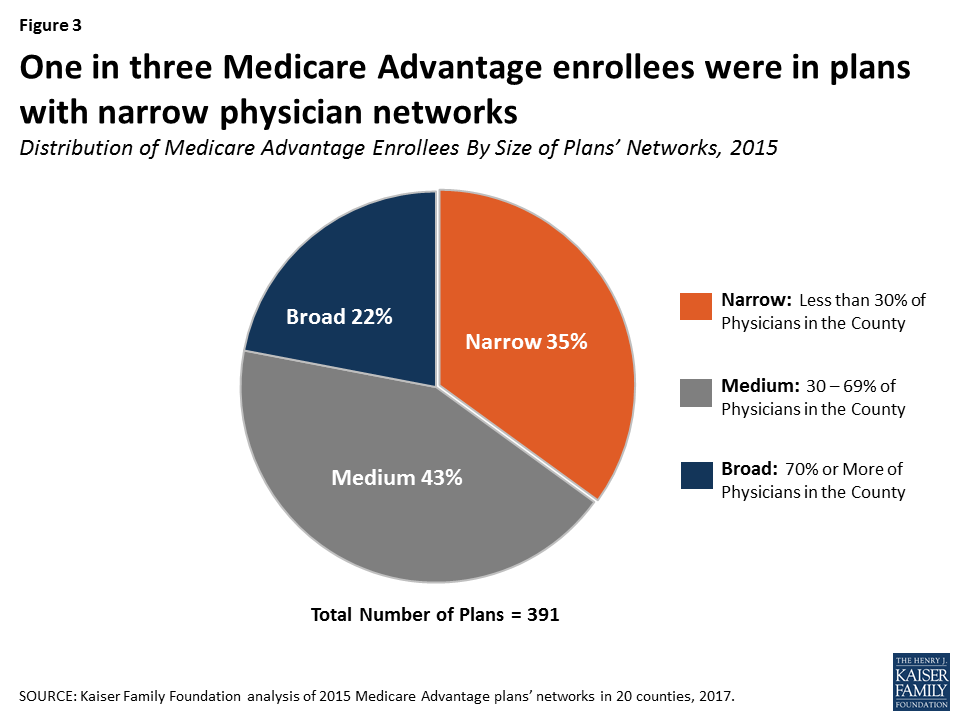

Medicare Advantage plans differ on how much they limit their physician pools along a spectrum between “Broad” and “Narrow” networks. A 2017 Kaiser Family Foundation report includes two graphs illustrating the breakdown of plans as of six years ago:

To make matters worse, even if a patient checks to be sure his physician(s) is (are) included on the Medicare Advantage plan he purchases, that may not be true. A 2018 investigation by CMS discovered systemic inaccuracy. “With 48.7% of provider directory locations containing at least one inaccuracy, the directories have become unreliable.” [quote]

3. Delays in payment from Medicare Advantage plans are hurting hospitals, especially in rural America

When a patient receives treatment in a hospital, and the payment is delayed, that hurts the hospital. Keep in mind that hospital expenses increase about 5% annually, but their revenues increase at only 3%. [source] In January, hospitals industrywide began the year with an operating margin index of -3.4%. [source] The economic strain is particularly harsh on hospitals with 25 or fewer beds (with a median operating margin of nearly -6% in 2021). [source]

Most small hospitals are in rural America, so the financial tightwire is most hazardous in less populated regions. Between 2010 to 2020, 136 rural hospitals closed in America. [source]

Given the razor-thin margins, hospitals can’t afford long delays in payment for expensive procedures such as an MRI or surgery. Compounding that stress, Medicare Advantage plans’ “onerous and duplicative clinical documentation” requirements (part of their Utilization Management process) taxes limited staff and resources, particularly in small hospitals. [source]

It is easy to understand why “Medicare Advantage plans appear to be among the worst payers at small rural hospitals.” [quote]

4. There is a lot of fraud in billing for Medicare Advantage plans

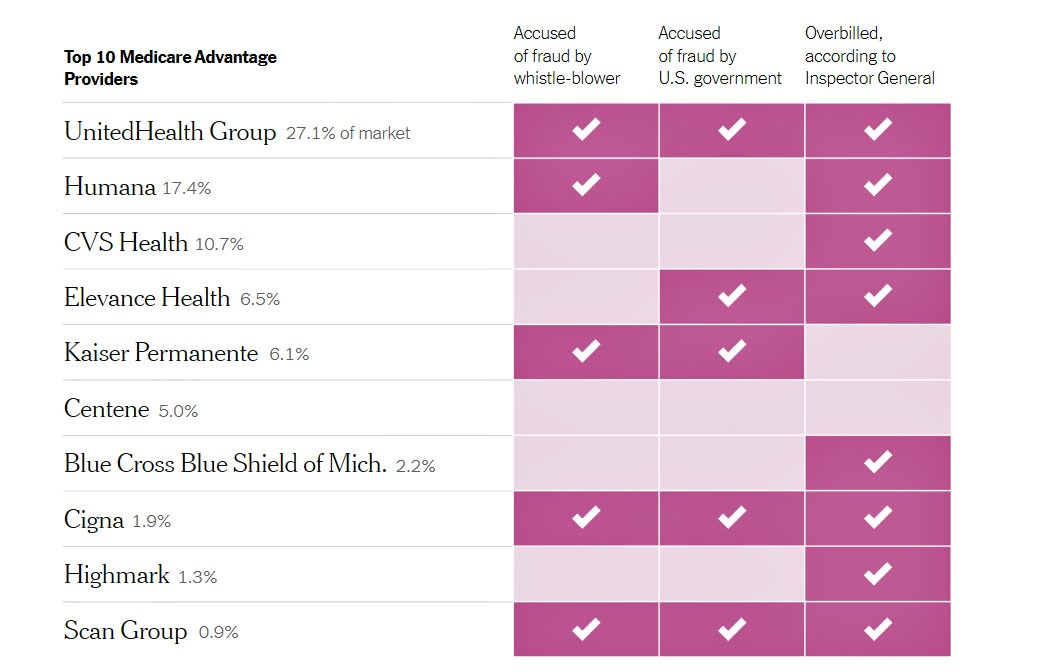

“The National Heath Care Anti-Fraud Association estimates conservatively that health care fraud costs the nation about $68 billion annually.” [quote, emphasis added] MedicareAdvantage.com, one of the country’s largest sellers of MA plans, details four types of fraud rampant in Medicare Advantage on their website. Still, none of their examples point to the fraud occurring within the private insurance companies themselves. The federal government has sued four of the five largest Medicare Advantage plans for fraud. [source]

Last October, the New York Times provided a visual consolidation of the extent of the problem [available here]:

Throughout this series, I have been trying to avoid the mind-numbing calculations determining the monthly per beneficiary reimbursement (“Capitated Rate”) the federal government pays a Medicare Advantage plan. (Here are two resources for readers that want to know more: #1- go here for an explanation of how those capitated rates are determined, #2- go here for a more detailed analysis.)

However, for the purposes of this discussion, all that is important to know is that in addition to the “Capitated Rate,” Medicare Advantage plans are paid an extra amount for a beneficiary with a higher level of illness or infirmity, in anticipation of that person’s medical expenses. [source]

The extra money available has apparently been low-hanging fruit for private insurance companies that want to increase the (already significant) profits from their Medicare Advantage plans.

An in-depth report from NPR (available here) explains how easy it has been for MA companies to claim a higher “risk score” for their patients, especially in cases involving diabetes with complications, major depression, and congestive heart failure.

You may be shaking your head, wondering: the plans denying coverage and dismissing the medical needs of their beneficiaries are also overstating their patients’ needs to get more money from the government? Yep.

Kaiser Family Foundation sued the government to gain access to 90 federal audits of the largest Medicare Advantage plans in 2011, 2012, and 2013 and reported their findings this January. [source]

As revealed by Kaiser, government auditors reviewed medical records for patients covered by these plans to see if the patients had the medical conditions reported by the Medicare Advantage companies. The results demonstrated extensive fraud. This table reveals the top three perpetrators; the findings from all 42 insurance companies audited are available here.

| Company | # of Audits | # of Patient Records Audited | Total Overpayment to the MA Plan |

| Humana | 11 | 2,211 | $2,965,323 |

| Cigna | 9 | 1809 | $1,737,505 |

| Aetna Inc. | 6 | 1206 | $1,274,399 |

The numbers reflected in these audits represent only a sampling of patient records. Still, from these files alone, “CMS officials have said they expect to collect more than $600 million in overpayments from the audits.” [quote]

Estimates are that when investigations on these companies spread further, the amount of overpayments the federal government “clawbacks” from Medicare Advantage plans could approach $3 billion. [source]

As you read these numbers, I hope you will remember that it is our taxpayer money we are talking about!

5. Medicare Advantage does not save money, at times has cost taxpayers more than traditional Medicare, and sends taxpayer money to people who are shareholders in private insurance companies (rather than pay for beneficiaries’ care)

I started addressing this fifth complaint in Part II of this series. This quote bears repeating:

“Historically, one goal of the Medicare Advantage program was to leverage the efficiencies of managed care [i.e., utilization management] to reduce Medicare spending. However, the program has never generated savings relative to traditional Medicare. In fact, the opposite is true.”

Kaiser Family Foundation [8/17/21] available here

For example, in 2019, U.S. taxpayers paid $321 more for every person who chose a Medicare Advantage plan rather than staying with traditional Medicare. [source]

The disparity in cost is not new. In 2010 the Affordable Care Act [“Obamacare”] aimed to equalize the federal outlay for traditional Medicare and Medicare Advantage plans [source], but:

“Payment neutrality has not yet been achieved between Medicare Advantage and traditional Medicare…. This inequity is estimated to have amounted to payments of an additional 2 percent to 4 percent per year to plans from 2010 to 2017.”

The Commonwealth Fund [12/8/17] available here

Both sources cited in these quotes will explain in great detail the failure of Medicare Advantage to reduce the cost of caring for senior Americans, as envisioned by President Clinton in 1997. [see Part II]

The question isn’t “Does Medicare Advantage work?” That answer is clearly “No.”

The critical question is, “Why are we spending more money to provide worse care to Americans over the age of 65?”

That is a question to ask your legislators in your state and D.C.

Conclusion

I set out on February 16th to explain Medicare Advantage and why I think it is both deceiving the beneficiaries who opt out of traditional Medicare and negating this promise we made as a country to our seniors in 1965:

“President Lyndon Johnson signed legislation creating Medicare… with a pledge that seniors no longer would ‘be denied the healing miracle of modern medicine.’” [quote]

At this point in this series, you may be convinced you want to choose traditional Medicare for yourself and your loved ones.

But do you have that choice? Most people I know approaching (or over) the age of 65 assume that their choice for coverage is theirs. They believe that can’t be denied under the Medicare promise of “guarantee issue.”

Increasingly, that isn’t true. Watch for Part IV of this series to understand why!

Want to Know More?

A volunteer for Grants for Seniors recently contacted me and asked me to include information about their organization in this Fontenotes series.

Here is her introduction:

We are volunteers working on this website to guide seniors and retirees when they need help. Our help subjects may be categorized as

Financial Help

Health Care

Help with Rent

Housing Assistance

Food Assistance

Clothing Assistance

Transportation Assistance

Daily Life and so on

We have covered many resources in all 50 states and now working on the biggest 200 cities to help elderly citizens reach easily to benefits where they live in. We have big goals on this site like building directories of programs and benefits in many categories.

I’ve gone to their website [https://grantsforseniors.org/

Thank you Rachel for reaching out!